How is working capital Calculated

What is working capital?

Working capital is the difference between a company’s current assets and current liabilities. It is a financial measure, which calculates whether a company has enough liquid assets to pay its bills that will be due within a year. When a company has excess current assets, that amount can then be used to spend on its day-to-day operations.

Current assets, such as cash and equivalents, inventory, accounts receivable, and marketable securities, are resources a company owns that can be used up or converted into cash within a year.

Current liabilities are the amount of money a company owes, such as accounts payable, short-term loans, and accrued expenses, that are due for payment within a year.

Positive vs negative working capital

Having positive working capital can be a good sign of the short-term financial health of a company because it has enough liquid assets remaining to pay off short-term bills and to internally finance the growth of its business. Without additional working capital, a company may have to borrow additional funds from a bank or turn to investment bankers to raise more money.

Negative working capital means assets aren’t being used effectively and a company may face a liquidity crisis. Even if a company has a lot invested in fixed assets, it will face financial challenges if liabilities come due too soon. This may lead to more borrowing, late payments to creditors and suppliers and, as a result, a lower corporate credit rating for the company.

When negative working capital is ok

Depending on the type of business, companies can have negative working capital and still do well. Examples are grocery stores like Walmart or fast-food chains like McDonald’s that can generate cash very quickly due to high inventory turnover rates and by receiving payment from customers in a matter of a few days. These companies need little working capital being kept on hand, as they can generate more in short order.

Products that are bought from suppliers are immediately sold to customers before the company has to pay the vendor or supplier. In contrast, capital-intensive companies that manufacture heavy equipment and machinery usually can’t raise cash quickly, as they sell their products on a long-term payment basis. If they can’t sell fast enough, cash won’t be available immediately during tough financial times, so having adequate working capital is essential.

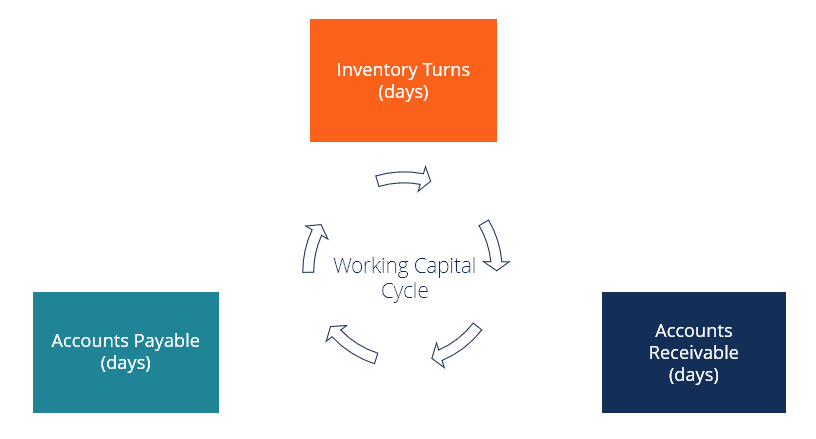

Learn more about a company’s Working Capital Cycle, and the timing of when cash comes in and out of the business.

Adjustments to the working capital formula

While the above formula and example are the most standard definition of working capital, there are other more focused definitions.

Examples of alternative formulas:

- Current Assets – Cash – Current Liabilities (excludes cash)

- Accounts Receivable + Inventory – Accounts Payable (this represents only the “core” accounts that make up working capital in the day-to-day operations of the business)